Nearly Limitless Options

in One IRA

Invest in both traditional and alternative assets with a single custodian – ready to go beyond a self-directed IRA?

Investor Insights Blog|Everything You Need to Know About the 10x Power of the Solo 401(k)

Small Business Plans

If you’re looking to boost your investment buying power or save for retirement exponentially faster, a Solo 401(k) (also known as an Individual 401(k) or Self-Employed 401(k)) offers an opportunity not available with other accounts.

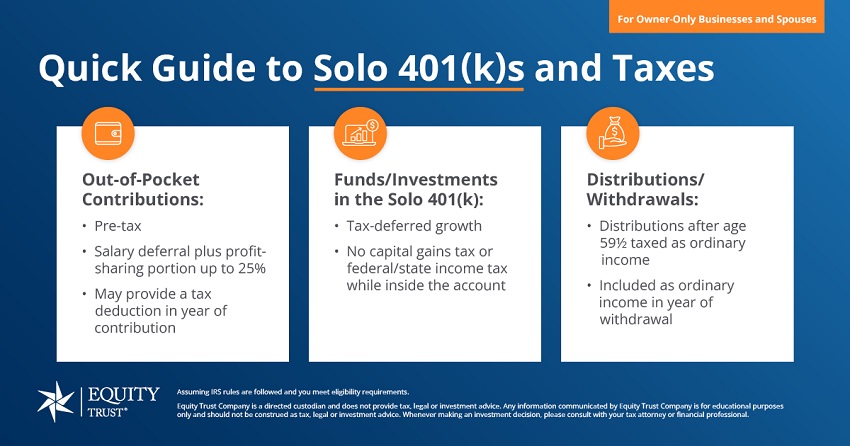

The account, designed for savers who are self-employed or a sole proprietor (including those who have an LLC), could help you super-charge your investing and claim larger tax deductions. Your business entity would be the sponsor of the plan, and it allows you as the employer and the employee to make contributions and salary deferrals into the account much higher than most other retirement plans.

However, the Solo (k) plan includes a couple of caveats, and it’s important to know the guidelines before getting started.

With a Solo 401(k) you could contribute nearly 10 times the amount you can with an IRA.

The contribution limit for a Traditional or Roth IRA in 2024 is $7,000, or $8,000 if you’re age 50 and older.

With an Individual (k), the employee (you) may defer 100 percent of your earned income, up to $23,000 per year, $30,500 if you’re 50 and older in 2024.

The employer (also you) may provide a profit sharing contribution of up to 25 percent of your income (20 percent for unincorporated entities).

For 2024, that’s a total contribution possibility of $69,000 if you’re under 50, or a whopping $76,500 if you’re 50 or older!

Higher contribution limits mean you’re able to claim higher tax deductions. That’s a potential $69,000 tax deduction if you’re under 50 and maxed out your contributions!

One important note, though: unlike IRAs and other accounts, the account must be established and employee salary deferrals must be made by December 31 to count for that tax year.

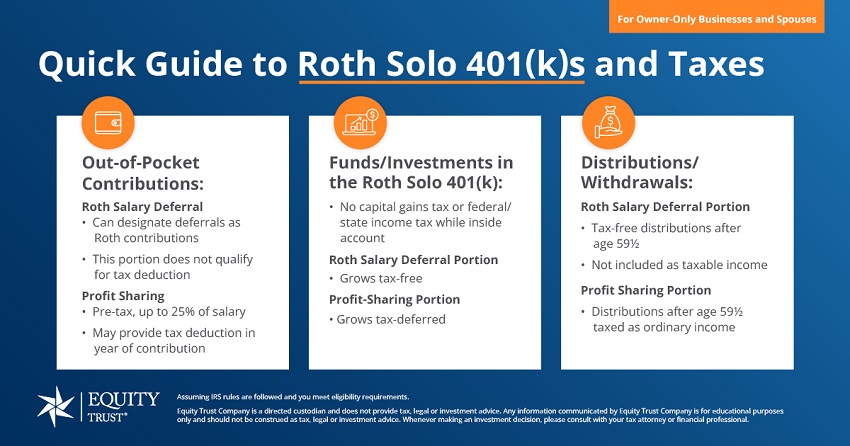

The Solo (k) has the added option of a Roth component. You can choose to make after-tax deferrals, which means future withdrawals are tax-free.

Plus, unlike a Roth IRA, there are no income restrictions associated with a Roth Solo 401(k).

The power of a self-directed Solo 401(k) is that you’re not limited to stock, bond, and mutual fund investments. This greatly expands your investment options to include real estate, private equity, precious metals, and much more. Self-directed investing is possible with custodians, such as Equity Trust, who are equipped to handle the unique recordkeeping requirements.

Suppose you want to purchase a rental property with your retirement account. If you’re contributing as much as $69,000 into your account each year ($76,500 for those 50 and older), think of how much quicker you’ll be able to accrue enough for the purchase than if you were contributing $7,000 or $8,000 to a self-directed IRA each year.

To be eligible for an Individual (k), you must be self-employed, have no other employees besides your spouse, and have active earned income in the business entity sponsoring the plan.

There are other qualifications as well. It’s important to review your eligibility with your CPA or financial professional.

If you find you don’t qualify for a Solo 401(k), there are several other options available to help you reach your retirement goals.

If you’re a small business owner, a SEP IRA or SIMPLE IRA may be your best course of action. A traditional or Roth IRA are also options for those who receive earned income and meet the qualifications.

You should consider all the pros and cons of the Solo (k) before making a decision. For example, be aware that if your Solo 401(k) invests through an LLC, you are liable for Unrelated Business Income Tax (UBIT).

UBIT is incurred when an investment made by a tax-exempt account receives income that passes through an LLC. The income is taxed using the trust and estate tax schedule.

Many investors choose to live with UBIT, believing the benefit of the investment ROI to far outweigh the cost of the tax. Discuss your scenarios with your tax professional to determine what’s best for you.

VIDEO: Solo K Pros and cons

Once you and your financial or tax professional determine if you’re eligible and could benefit from an Individual (k), you’re ready to find a provider to open the account.

A few things to consider when you shop for providers:

[Read more: Tips for Finding a Custodian.]

To receive the full benefits of the Solo 401(k) in 2024, it’s important to open the account before the end of the year. The employee portion of the contribution must be made by the end of 2024 to count for the 2024 tax year.

In addition, custodians have their own account establishment deadlines that may differ from the IRS deadline. At Equity Trust, for example, you typically must have your application completed by December 21 to open the account in that year.

We’re here to answer your questions about eligibility and account setup and maintenance. Claim your free guide or call 888-382-4727 to speak to a knowledgeable IRA Counselor.

What is UBIT or UBTI?

Am I eligible to make a contribution? How much can I contribute?

1 Equity WayWestlake, OH 44145

Terms of UsePrivacy PolicySite Map

© 2024 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 6/1/2024. 1ici.org, total assets in IRAs as of 12/2023

Terms of UsePrivacy PolicySite Map

© 2024 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 6/1/2024. 1ici.org, total assets in IRAs as of 12/2023

You are leaving trustetc.com to enter the ETC Brokerage Services (Member FINRA/SIPC) website (etcbrokerage.com), the registered broker-dealer affiliate of Equity Trust Company. ETC Brokerage Services provides access to brokerage and investment products which ARE NOT FDIC insured. ETC Brokerage does not provide investment advice or recommendations as to any investment. All investments are selected and made solely by self-directed account owners.

Continue

Browse platforms and providers in private equity, cryptocurrency, lending, real estate, and precious metals asset classes – all in one place.